Brownian motion (布朗運動)

定義: Brownian motion

定義 (in Shreve, Stochastic Calculus for finance)

- (Ω,F,P) is probability space.

- For each ω∈Ω, suppose there is a continuous function W(t), t≥0, which satisfies W(0)=0 and depends on ω.

- Then W(t), t≥0 is Brownian process if ∀0=t0<t1<⋯<tn, the increment W(t1)−W(t0), W(t2)−W(t1), \cdots W(tn)−W(tn−1 are mutual independent.

- Each of the increment is i.i.d. random variable of N(0,ti+1−ti)

- E(W(ti+1)−W(ti))=0.

- Var(W(ti+1)−Wti)=ti+1−ti.

- ∴W(t)=W(t)−W(0)∼N(0,t).

Filtration

- (Ω,F,P) is probability space, and Brownian process W(t), t≥0.

- A filtration for Brownian process is a collection of σ-field F(t), t≥0 satisfies:

- Information accumulates (增大資訊集合), 0≤s≤t, F(s)⊆F(t).

- There is at least much information available at the later time F(t) as there is at the earlier time F(s).

- 資訊為擴增的集合。

- Adaptivity (適應性), ∀t≥0, {w∣W(t,ω)}∈F(t) or called W(t) is F(t)-measurable.

- The information available at time t is sufficient to evaluate the Brownian process W(t) at this time.

- 現在的事件必須可以用到目前為止的資訊集合評估。

- Independence of future increment, 0≤s≤t, P(W(t)−W(s)∣F(s))=P(W(t)−W(s)).

- Any increment of the Brownian process after time t is independent of the information available at time t.

- 未來的事件與現在的資訊集合獨立,即無法預測Brownian過程未來之值。

- Properties (1) and (2) guarantee that the information available at teach time t is at least as much as one would learn from observing the Brownian motion up to time t.

- There are two possibilities for the filtration F(t) for Brownian process.

- F(t) contains only the information obtained by observing the Brownian process itself up time t.

- If the information F(t) includes observations of processes other than Brown process W(t), this additional information is not allow to give clues about the future increments of W because of the property (3).

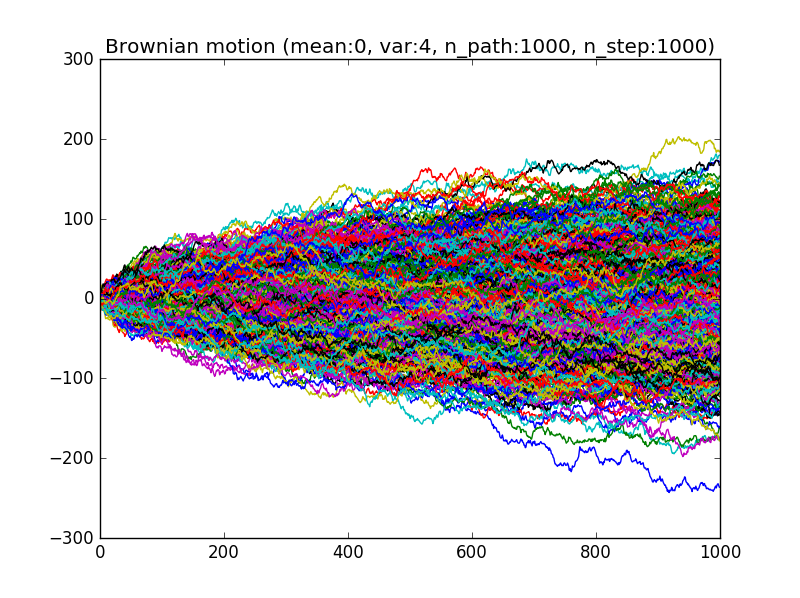

Implementation

import numpy as np

import matplotlib.pyplot as plt

def brownian_motion(n_path, n_step=1000, mean=0, variance=1):

points = np.random.randn(n_path, n_step)*np.sqrt(variance) + mean

return(np.cumsum(points, axis=1))

n_path, n_step, mean, variance = 1000, 1000, 0 , 4

paths = brownian_motion(n_path, n_step, mean, variance)

for rdx in xrange(n_path):

plt.plot(paths[rdx])

plt.title("Brownian motion (mean:{}, var:{}, n_path:{}, n_step:{})".format(

mean, variance, n_path, n_step))

plt.show()

標準布朗運動性質

B(t)∼N(0,t).

{B(t),t ≥0} are a standard Brownian process,0<s<t,a,b∈R.

- Cov(B(s),B(t))=E(B(s),B(t))=s,∀s≤t.

∵Cov(B(s),B(t))====Cov(B(s),B(s)+B(t)−B(s))Cov(B(s),B(s))+Cov(B(s),B(t)−B(s))[indep. incr.]Cov(B(s),B(s))+0s.

- Var(B(s)−B(t))=t−s, Var(B(t))=t.

- Var(aB(s)+bB(t))=(a+b)2s+b2(t−s).

∵Var(aB(s)+bB(t))====Var(aB(s)+b(B(s)+B(t)−B(s)))Var((a+b)B(s)+b(B(t)−B(s)))Var((a+b)B(s))+Var(b(B(t)−B(s))[indep. incr.](a+b)2s+b2(t−s).

- aB(s)+bB(t)∼ normal distribution.

- Covariance matrix of (W(t1),W(t2),⋯,W(tn)) is

⎣⎡E(W2(t1))⋮E(W(tn)W(t1))⋯⋱⋯E(W(t1)W(tn))⋮E(W2(tn))⎦⎤

The density function

- ft(x)=√2πt1e−2tx2.

The joint pdf

f(x1,x2,⋯,xn)==ft1(x1)ft2(x2−x1)⋯ftn−tn−1(xn−xn−1)(2π)n/2[t1(t2−t1)⋯(tn−tn−1)]1/21exp{−21[t1x12+t2−t1(x2−x1)2+⋯+tn−tn−1(xn−xn−1)2]}

Conditional distribution

Covariance

X(t), t≥0 is Brownian process, X(t)∼N(0,σ2t).

- 0<s<t, Cov(X(s),X(t)=σ2s.

Cov(X(s),X(t))=====E(X(s)X(t))E(X(s)(X(s)+X(t)−X(s)))Var(X(s))+Cov(X(s),X(t)−X(s))Var(X(s))σ2s.

- Generally, Cov(X(s),X(t))={σ2min(∣s∣,∣t∣)0st>0,st<0.

Correlation

- Corr(X(s),X(t))=√st, 0<s<t.

Corr(X(s),X(t))===√Var(X(s))Var(X(t))Cov(X(s),X(t))√σ2sσ2tσ2s√st.

平賭(鞅)(Martingle process)

(Ω,F,Fn,P) be a probability space, and Fn is a flitration.

- If X(t)∈Ft-measurable, E(∣X(t)∣)<∞, and

- X(t)=E(X(t+1)∣Ft).

- then X is a martingale process.

X(t) is a Brownian process, X(t)∼N(0,σ2t), the following are martingale processes:

- X(t)

- X2(t)−σ2t

- (Exponential martingale process) exp{μX(t)−2μ2σ2t}, μ∈R.

X(t) is martingale process.

0<s<t, X(t)=X(t)−X(s)+X(s).

E(X(t)∣F(s))(∵X(t)−X(s) indep. to Fs)====E(X(t)−X(s)+X(s)∣F(s))E(X(t)−X(s)∣F(s))+E(X(s)∣F(s))E(X(t)−X(s))+X(s)X(s).

X2(t)−σ2t is martingale process.

X2(t)==(X(t)−X(s)+X(s))2(X(t)−X(s))2+2X(s)(X(t)−X(s))+X2(s)

E((X(t)−X(s))2∣Fs)=E((X(t)−X(s))2)=(t−s)σ2.

E(X2(s)∣Fs)=X2(s).

∴E(X2(t)−σ2t∣Fs)=(t−s)σ2+X2(s)−σ2t=X2(s)−σ2s.

exp{μX(t)−2μ2σ2t}, μ∈R. is martingale process.

- μX(t)=μ(X(t)−X(s))+μX(s).

- E(exp(μX(t))∣Fs)=exp(μX(s))⋅E(exp(μ(X(t)−X(s)))).

∵ X(t)−X(s)∼N(0,(t−s)σ2),

- the mgf E(exp(μ(X(t)−X(s)))=exp(2μ2(t−s)σ2).

∴E(exp(μX(t)−2μ2σ2t)∣Fs)==exp(μX(s)+2μ2(t−s)σ2−2μ2σ2t)exp(μX(s)−2μ2σ2s).

Shift property

X(t), t≥0 is Brownian motion, X(t)∼N(0,σ2t).

- ⇒ Y(t)=X(t+r)−X(r), ∀r∈R is Brownian process.

E(Y(t))=E(X(t+r)−X(r))=E(X(t+r))−E(X(r))=0.

Cov(Y(t),Y(s))=σ2min(t,s).

Cov(X(t),X(s))=====E(X(t)X(s))E((X(t+r)−X(r))(X(s+r)−X(r))E(X(t+r)X(s+r))−E(X(t+r)X(r))−E(X(r)X(s+r))+E(X2(r))σ2min(t+r,s+r)−σ2r−σ2r+σ2σ2min(t,s).

Y(t) is normal distribution.

Scaling property

X(t), t≥0 is Brownian motion, X(t)∼N(0,σ2t).

- ⇒ Y(t)=cX(c2t), ∀c>0 is Brownian process.

- E(Y(t))=0.

Cov(Y(t),Y(s))=σ2min(t,s).

Cov(X(t),X(s)===c−2E(X(c2t)(c2s))σ2c−2min(c2t,c2s)σ2min(t,s).

- Y(t) is normal distribution.

Brownian motion with drift

前面討論的Brownian motion都是沒有趨勢,即E(X(t))=0, ∀t.

X(t), t≥0 is Brownian process with drift coefficient μ and variance parameter σ2 if

- X(0)=0.

- X(t), t≥0 has stationary and independent increments.

* X(t)∼N(μt,σ2t).

等價定義, B(t), t≥0 is standard Brownian process and X(t)=σB(t)+μt.

Geometric Brownian proces

- Y(t), t≥0 is Brownian process, and Y(t)∼N(μt,σ2t).

Defintion: Geometric Brownian motion

- X(t)=eY(t), t≥0.

- i.e. lnX(t)=Y(t)∼N(μt,σ2t).

E(X(t)∣X(u),0≤u≤s)=X(s)E(eY(t)−Y(s)).

E(X(t)∣X(u),0≤u≤s)(∵indep. incr.)====E(eY(t)∣X(u),0≤u≤s)E(eY(t)−Y(s)+Y(s)∣X(u),0≤u≤s)eY(s)E(eY(t)−Y(s)∣X(u),0≤u≤s)X(s)E(eY(t)−Y(s)).

Standard Brownian bridge process

Standard Brownian bridge process為起點與終點在相同位置的隨機過程。

B(t), t≥0 is standard Brownian process, B(t)∼N(0,t).

Let Y(t)=B(t)−tB(0), 0≤t≤1.

- Y(0) = B(0) - 0 B(1) = 0.

- Y(1) = b(1) - B(1) = 0‧

- Standard Brownian bridge from Y(0)=0 to Y(1)=0.

Standard Brownian bridge process properties

- E(Y(t))=E(B(t)−tB(0))=0.

Cov(Y(t),Y(s))=s(1−t), 0<s<t<1.

Cov(Y(t),Y(s))====Cov(B(t)−tB(1),B(s)−sB(1))Cov(B(t),B(s))−sCov(B(1),B(t))−tCov(B(s),B(1))+stCov(B(1),B(1))s−st−st+sts(1−t).

Brownian bridge process

B(t), t≥0 is standard Brownian process, B(t)∼N(0,t).

Process start from a at time t=0, achieve to b at t=T.

* Y(t)=a(1−Tt)+bTt+(B(t)−TtB(t)), 0≤t≤T.

* {% math %}Y(0) = a{% endmath %}.

* {% math %}Y(T) = b{% endmath %}.

- E(Y(t))=a(1−Tt)+bTt.

Var(Y(t))=t(1−Tt).

Var(Y(t))====E(B(t)−TtB(t))2E2(B(t))−T2tE(B(t)B(T))+T2t2E2(B(T))y−T2t2+T2t2Tt(1−Tt).

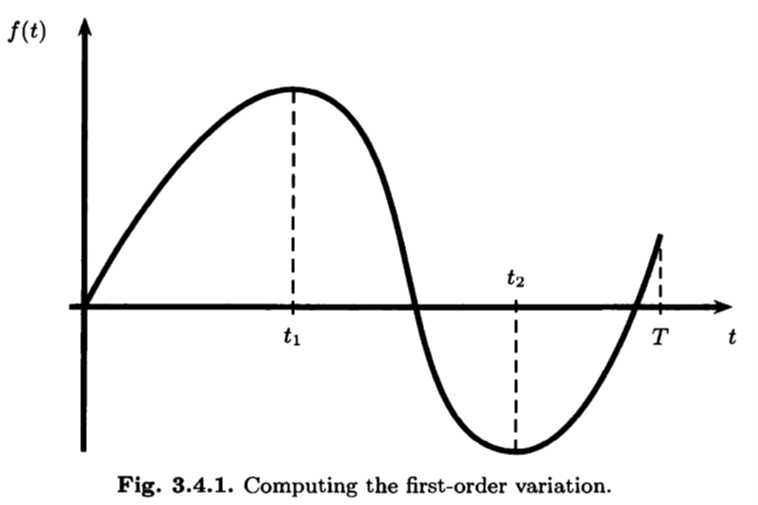

First-order variation

- 上圖中,依點t1, t2至T的函數變動量為FVT(f)=(f(t1)−f(t0))+(f(t2)−f(t1))+(f(T)−f(t2))=∫0t1f′(t)dt+∫t1t2−f′(t)dt+∫t2Tf′(t)dt=∫0T∣f′(t)∣dt.

- Let partition π={t0,t1,⋯,tN} of [0,T], and δ=max0≤k≤N(tk+1−tk).

- Define FVT(f)=limδ→0∑k=0N−1∣∣f(tk+1)−f(tk))∣∣.

- By mean-value-theorem (MVT) of derivative

- ∃k∈tk∗∈[tk,tk+1]∋tk+1−tkf(tk+1)−f(tk))=f(1)(tk∗).

- ∴f(tk+1−f(tk))=f(1)(tk∗)(tk+1−tk).

- ∑k=0N−1f(tk+1)−f(tk)=∑k=0N−1∣∣f(1)(tk∗)∣∣(tk+1)−tk).

- ∴limδ→0∑k=0N−1∣∣f(tk+1)−f(tk)∣∣=limδ→0∑k=0N−1∣∣f(1)t(k∗)∣∣(tk+1−tk)=∫0T∣∣f(1)(tk∗)∣∣dt.

- ∴FVT(f)=∫0T∣∣f(1)(tk∗)∣∣dt. (QED)

Quadratic variation

- The quadrativ variation of fucntion f up to time T is

[f,f](T)=δ→0limk=0∑N−1(f(tk+1)−f(tk))2

- Suppose f∈C1([0,T]) (i.e. f has a continuous 1st derivative)

∑k=0N−1(f(tk+1)−f(tk))2≤δ∑k=0N−1∣∣f(1)(tk∗)2∣∣(tk+1−tk).

[f,f](T)≡≤==δ→0limk=0∑N−1(f(tk+1)−f(tk))2δ→0lim(δk=0∑N−1∣∣f(1)(tk∗)2∣∣(tk+1−tk))δ→0limδδ→0limk=0∑N−1∣∣f(1)(tk∗)2∣∣(tk+1−tk)δ→0limπ∫0T∣∣f(1)(t)∣∣2dt

If limδ→0π∫0T∣∣f(1)(t)∣∣2dt≤∞ then [f,f](T)=0.

If limδ→0π∫0T∣∣f(1)(t)∣∣2dt→∞, then [f,f](T) diverges.

Brownian process is continuous, but not differentiabl everywhere, therefore the MVT is failed!!